Management that takes into account capital costs and stock prices (financial and capital strategy)

Further improving equity spreads,

Meeting the expectations of shareholders and investors

For information on the Itoki Group‘s actions to achieve cost of capital and stock price conscious management, as well as a collection of financial and non-financial data, please refer to the following.

Financial and capital strategies that take capital costs into consideration

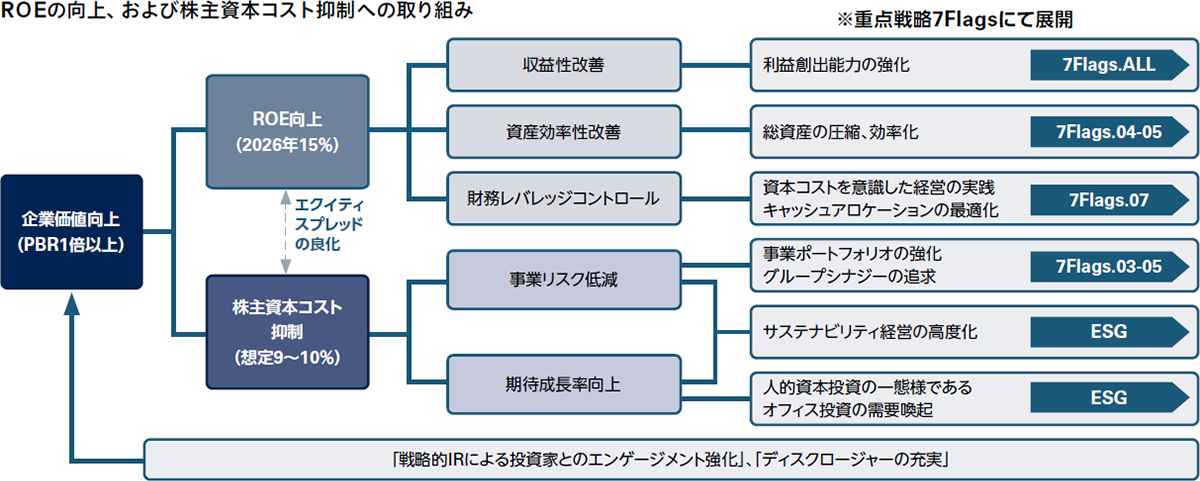

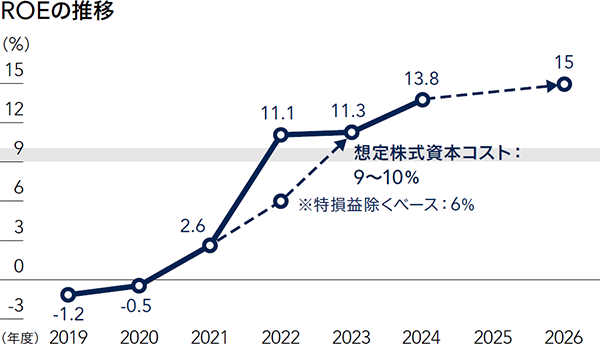

Itoki's basic financial and capital strategy is to increase corporate value with an awareness of capital costs. We have set a high expected cost of shareholders' equity (CAPM) of 9-10%. Based on this premise, we aim to meet the expectations of shareholders and investors at a high level and expand our equity spread. In order to do so, we are aiming for an ROE of 15%, an operating profit margin of 9%, and absolute sales and operating profit of 150 billion yen and 14 billion yen in fiscal 2026, the final year of our medium-term management plan, "RISE TO GROWTH 2026," which we position as the high-profit phase.

Itoki is also working to further improve its equity spread in line with its 7 Flags and ESG strategies, which are key strategies in its current medium-term management plan. Itoki previously missed its earnings forecast for six years, resulting in a continuous decline in its stock price. For this reason, it is strongly committed to achieving the numbers it has committed to, and is working to improve the accuracy of its forecasts.

Review of performance for fiscal year 2024

In fiscal year 2024, we are capturing demand for renovations and office relocations, resulting in a third consecutive year of increased sales, with sales reaching 138.4 billion yen (up 4.1% from the previous year). Furthermore, thanks to the success of our structural reforms, we have achieved a record-high profit for the second consecutive year. Operating profit, in particular, increased by 1.5 billion yen from the previous year, reaching the long-awaited 10 billion yen mark. Gross profit increased by 2.9 billion yen, absorbing a 1.4 billion yen increase in selling and general administrative expenses due to wage increases, the reopening of our showroom and head office, and digital transformation investments. Gross profit increased by 2.1 billion yen, in proportion to sales, meaning profitability improved by approximately 800 million yen. By business segment, Equipment & Public Works-Related Business saw lower sales and profits due to project postponements, but our core Workplace Business drove the performance.

On the other hand, we recorded a provision of 150 million yen as compensation for past actual work performed by logistics companies, and 570 million yen to pay a penalty to our Singapore consolidated subsidiary, Turcus. However, we also recorded the gain on sale obtained through asset efficiency improvements as extraordinary income, resulting in net income of 7.1 billion yen (up 1.6% from the previous year). We are trying not to carry over the impact of the compliance issue, which caused inconvenience, into fiscal 2025.

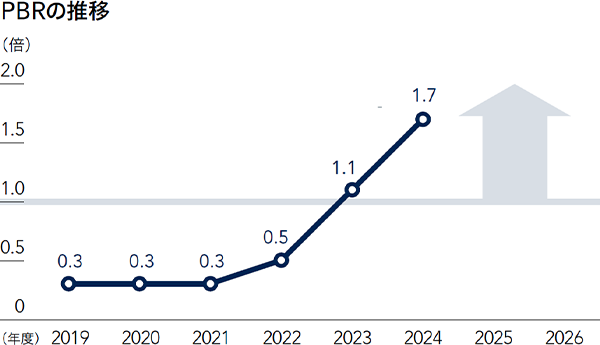

Regarding the balance sheet, intangible fixed assets increased due to digital transformation investments. Based on dialogue with capital markets, we conducted a share buyback and increased financial leverage. As a result, net assets decreased by 5.6 billion yen from the end of the previous fiscal year to 49.3 billion yen, and the equity ratio was 40.9% (down 5.0 points). Thanks to the effect of increasing financial leverage from 2.1x to 2.4x in the previous fiscal year and an improvement in the net income margin from 4.4% to 5.2%, ROE rose to 13.8% (up 2.5 points). The equity spread widened, and the price-to-book ratio (PBR) of the stock price rose to 1.7x. Furthermore, we increased dividends, significantly increasing total shareholder return (TSR). Regarding the stock price, not only the PBR but also the P/E ratio reached double digits. While not sufficient, we believe Itoki's growth potential is gradually being reassessed. We also place importance on financial stability, so we will manage leverage appropriately.

ROIC and business portfolio management

Itoki has set a hurdle rate for its business activities, i.e., weighted average cost of capital (WACC), at around 8%, and will increase ROIC from both the profit and loss statement and balance sheet perspectives. With regard to asset efficiency, we will continue to optimize our assets, including by reviewing cross-shareholdings and selling non-business assets.

ROIC for fiscal year 2024 is expected to be 9.1%. While ROIC by business segment remains a challenge, ROA by business segment was 12.2% for the Workplace business (up 1.4 points year-on-year), and 6.9% for Equipment & Public Works-Related Business (up 0.8 points year-on-year) (see 11-Year Financial and Non-Financial Data [830KB]). Going forward, we aim to establish a subscription model with "Office 3.0" and evolve into a business model with higher asset return. From fiscal year 2025 onward, we will focus on this point and aim to increase the profitability of Workplace Business. Therefore, while the profit composition of our business portfolio will become even more dependent on Workplace Business when viewed by business segment, we believe that the increased weight of "Office 2.0" and "Office 3.0" will improve stability. Furthermore, we are investing funds in the restructuring of Dalton, a consolidated subsidiary that accounts for more than half of the sales of the Facility Equipment and Public Business, so we expect the business portfolio to be strengthened by business segment under the next medium-term plan.

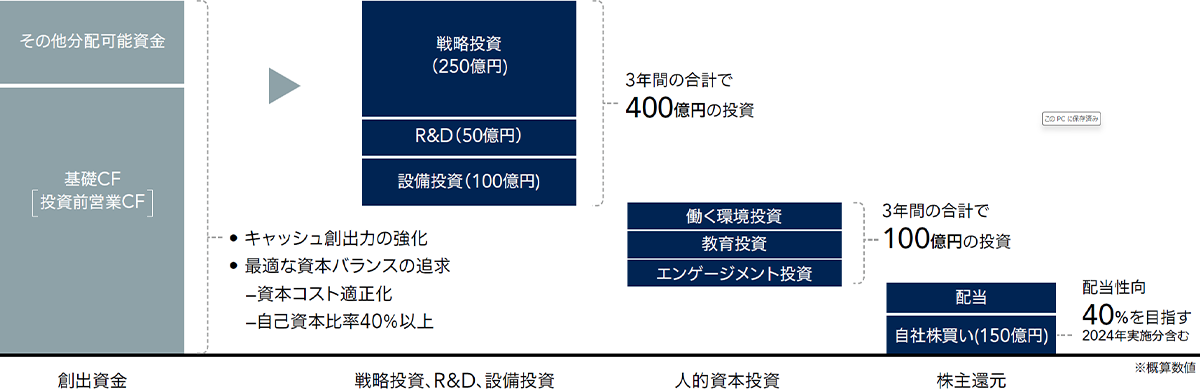

Cash allocation

In this mid-term plan, we have allocated 25 billion yen to strategic investments including M&A, 5 billion yen to R&D, and 10 billion yen to capital investments, with 10 billion yen allocated to human capital investments. We also plan to strengthen shareholder returns. With regard to investments, we will continue to invest in digital transformation aimed at improving business efficiency, and we are considering strategic investments in production facilities not only to address aging equipment but also to improve production efficiency. We will also consider strategic investments aimed at business expansion.

We are currently building a monetization model for the data business in the "Office 3.0" domain, with the goal of achieving sales of 3 billion yen in fiscal 2026. In addition to investing in these new businesses that are expected to contribute to future revenue, we will also consider optimal investment allocation, with an eye toward strengthening our business portfolio through M&A. With regard to strategic investments, we intend to carefully analyze risks and make investments that emphasize returns.

Operating cash flow for fiscal year 2024 was minus 1 billion yen due to the complete elimination of notes payable during the previous fiscal year and the shortening of payment terms in accordance with the Subcontract Act, but we expect the cycle to level out by fiscal year 2025. Regarding the balance sheet, we have begun company-wide initiatives for accounts receivable management and inventory management. We will also promote group management and review our cash management methods to maximize capital efficiency as a group. By shifting from the current system in which each subsidiary manages its own funds individually to a system that allows for group-wide fund management, we will aim to improve capital efficiency and cash flow.

By generating operating cash flow that exceeds growth investments, we believe it would be ideal to have positive free cash flow and secure stable funds for shareholder returns. However, Itoki is in a period of major transformation, and we do not believe it is wise to curb investments for growth. Therefore, we will manage our finances so that we can properly allocate funds to growth investments while maintaining financial soundness from short-, medium-, and long-term perspectives.

Obtaining a credit rating and takeover defense measures

In fiscal 2024, we obtained a credit rating. As a result, we received a high rating of single A minus from R&I, due to improved profitability. In addition, as our financial position has strengthened and our market capitalization has increased, we have belatedly abolished our takeover defense measures.

Financial outlook for fiscal year 2025

For fiscal year 2025, we are targeting sales of 145 billion yen (up 4.7% year-on-year) and operating profit of 11.5 billion yen (up 14.1% year-on-year). In particular, we expect operating profit for Workplace Business to increase 19.3% to 9.6 billion yen. Given the current state of business negotiations, we expect sales to continue to expand, and we believe that a rise in the proportion of "Office 2.0" and the addition of "Office 3.0" will further enhance profitability. On the other hand, although we are seeing positive demand, we are forecasting operating profit for Equipment & Public Works-Related Business to decrease 3.1% to 1.8 billion yen, as we expect labor shortages in the construction industry and rising material prices to lead to prolonged delivery delays.

Shareholder returns and economic value

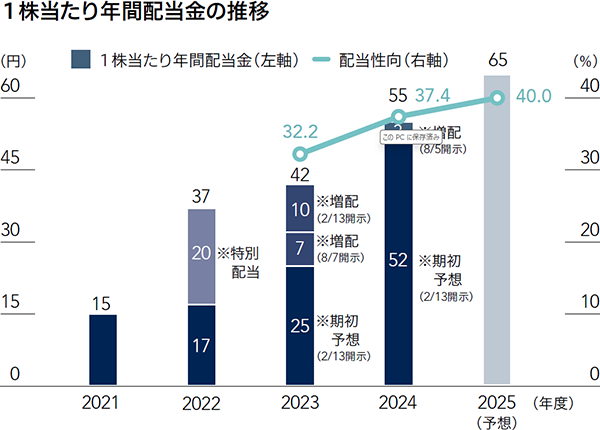

For shareholder returns in fiscal 2024, we have raised the dividend payout ratio to 37.4% due to the expansion of net income, and set the annual dividend per share at 55 yen (an increase of 13 yen from the previous fiscal year). For fiscal 2025, we will raise the dividend payout ratio target to 40% ahead of schedule, aiming for an annual dividend of 65 yen. We intend to flexibly implement share buybacks based on our cash generation capacity and financial situation.

Itoki plans to expand its business in the "Office 3.0" field and shift to a stock-based business, which it believes will reduce the risks posed to the business by changes in the office market environment. Furthermore, by strengthening business management by segment, it will improve the profitability and asset efficiency of the entire business portfolio and increase ROE. Itoki is drawing up an equity story that will significantly widen the equity spread and boost shareholder value.

- Investor Relations

- IR News

- Top message

- To all individual investors

- IR Policies

- Medium-term management plan

- Management that takes into account capital costs and stock prices (financial and capital strategy)

- Digital Transformation Strategy

- Shareholder returns

- Shareholder Benefit Program

- Corporate governance

- Disclosure policy

- Basic policy against anti-social forces

- IR resource room

- Performance/finance

- Stock information

- IR event

- Dialogue with shareholders (IR activities)

- FAQ